SHARED RESEARCH FACILITIES

Access shared resources

Discover More

FOR NORTHEASTERN FACULTY AND PARTNERS

Our research facilities are centralized

and shared to provide researchers and

partners with access to instruments,

technologies, services, expert

consultation and more.

Our shared research facilities

Our shared research centers include three categories of service centers, ordinary, shared instrumentation cores, academic service centers, and specialized service centers.

Valur Olaffson / Director

Boston Electron Microscopy Center

Srinivas Sridhar / Director

Division of Laboratory Animal Medicine

Sean Sullivan / Director

Expeditionary Cyber and Unmanned Aircraft System

Filip Cuckov / Director

Institute for Chemical Imaging of Living Systems

James Monaghan / Director

Kostas Advanced Nano-Characterization Facility

Wentao Liang / Director

Kostas Nanoscale Technology and Manufacturing Research Center

Sivasubramanian Somu / Director

Virginie Sjoelund / Associate Director

Nuclear Magnetic Resonance Facility

Jason J. Guo / Director

Frequently asked questions

Get answers to your questions about processes, costs, equipment maintenance, and more.

What is a Shared Research Facility (Core Facility)?

A Northeastern University Shared Facility is an operation that charges for goods or services in direct support of the research or academic mission of the university. Shared Facilities recover some or all their costs through fees charged to users, including federally sponsored projects, based on established billing rates and actual usage of service.

Northeastern recognizes four types of shared facilities:

- Specialized Service Facility (SSF) with operating expenses over $1 million

- Shared Research Facility with operating expenses over $100,000

- Department user/Resource Facility is the Shared Research Facility within a Department and with operating expenses below $100,000

- Auxiliary Service Unit (Recharge Center)

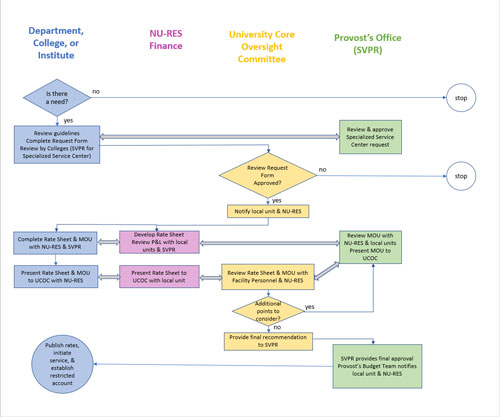

What is the process for establishing a Shared Research Facility (Core Facility)?

The flow chart of the review process is below. The detailed review process can be found in Administrative Guidelines from page 6 to page 7.

How should the Shared Research Facility (Core Facilities) set charges for users?

Shared Research Facility should set user fees based on actual costs and actual usages. The detailed process of rate setup is listed in the administrative guidelines. Please refer to the Administrative Guidelines for more details. The basic principle can help to develop the billing rate is here:

- User types must be defined

- Federal sponsored users will always get the lowest rate

- We can only recover the cost that was generated from operating the facility

- Cannot cross-subsidize between user groups

- External users may be charged higher rates that include the F&A costs of the Shared Facilities

Can one Shared Research Facility (Core Facilities) support another?

No. The goal for setting up the Shared Research Facility is to create a billing rate that does not cross-subsidize services or user groups. The separated billing rates should be established for each service that represents a significant activity of the shared research facility. The costs and revenues should also be separately identified for each service.

What are the typical allowable costs for determining a Shared Research Facility?

The expense budget should include all costs for operating the Shared Facilities, including administrative expenses directly associated with operations of the facility. Please refer to Cost Principle in UG for detailed information and UG Subpart E (§200.468) for Specialized Service Facility. Expense categories include:

- Salaries, wages, and fringe benefits

- Materials and supplies

- Maintenance and repair, including equipment maintenance agreements

- Rentals and leases, including operating equipment leases

- Travel and conferences relevant to training and service center management

- Purchased services/professional fees

- Administrative Guidelines also provide detailed information about allowable costs. Please see the page 8 and 9 of Administrative Guidelines for more detail.

What are the types of costs that are unallowable?

Unallowable costs must be excluded from the budget as well as the service center rate calculation and may not be charged to Service Center users. Examples of unallowable costs include, but are not limited to those listed below:

- Advertising

- Alcoholic beverages

- Airfare in excess of “coach”

- Bad debt or uncollected billings

- Capital equipment purchases

- Depreciation (Please see the depreciation FAQ below)

- Donations and contributions

- Entertainment/gifts

- Fines and penalties

- Memberships

- General office supplies

- Selling and marketing costs

- Sales tax

Can a Shared Research Facility (Core Facilities) generate a profit from internal users?

General internal users are typically the Federal government (sponsor agreements). Typically, we aim to reach the breakeven, but we understand this is not usually the situation. So, we set up an allowable variance threshold at +/- 15%. Any surplus should be carried forward as an adjustment to the billing rates of the following year or the next succeeding year. Any surplus over 15% should return to users. See NIH FAQ and Administrative Guidelines for more details.

Can depreciation be added to the costing plan?

Depreciation is generally considered an allowable cost. However, Northeastern University includes depreciation costs in F&A proposal. Therefore, we do not include the depreciation in the rate for Shared Research Facility.

Can my facility offer special discounted rates for internal high-volume users?

The same rate schedule must be available to all internal users, so it is not allowed to define a special class of high-volume internal users. However, it is possible to set a threshold number of service units, such that once any user exceeds the threshold, they are charged for the service at a discounted rate. Thus, high-volume users can realize an average discount for the service, even though the rate scheme is available to all users.

Not all equipment maintenance in my facility can be covered by service contracts. Can the facility accumulate funds to pay for incidental repairs and replacement parts?

Federal guidelines do not generally permit accumulation of facility revenues for specific purchases, although the cost of maintaining equipment in operating condition is allowable. The average annual cost of incidental maintenance may be budgeted in the rate sheet with a reasonable, well-documented estimate. Since such costs will likely occur at irregular intervals, Northeastern will allow facilities to carry over funds for incidental maintenance between financial periods and accumulate them up to a cap (which is typically twice the average annual cost, but may be negotiated). When accumulated funds for maintenance exceed the cap, the facility must reduce its rates or refund the excess maintenance costs to users. Accumulated maintenance funds may only be used for maintenance and replacement of existing parts, and not to acquire new equipment or accessories.

How can my facility acquire new equipment?

Support for acquisition of new research core equipment comes in several forms at Northeastern: (i) direct purchase from operating funds by a College, Department, Institute, or the Provost; (ii) direct purchase for a core by a College or Department with contribution from the Provost in association with the expressed needs of a faculty hire; (iii) cost sharing of equipment acquired via instrumentation proposals by the Provost with contributions from Colleges, Departments, or Institutes; (iv) purchase using a gift from a donor to Northeastern designated for this purpose; (v) in-kind donation of equipment to Northeastern from an industrial or academic partner.

Where can I find the NIH FAQ’s on Core Facilities?

You can find the NIH Core Facilities FAQ’s here.

Last updated on May 15, 2024

Stand-up documents

The Shared Research Facility Committee provides oversight, reviews proposals, analyzes, and approves the rates charged to users for their services. The director of the Shared Research Facility has responsibility for its operational and financial management. Please review the documentation for establishing a Shared Research Facility at Northeastern University:

Policy on Shared Research Facilities

Administrative guidelines for shared research facilities

Proposed facility setup flowchart

Northeastern shared research facility request form

Shared research facility-Memorandum-of-Understanding (MOU)

NU shared research facility rate sheet 3-year

QUICK LINKS

CAMPUS LOCATIONS

Today, a vanguard of donors is driving Northeastern’s historic $1.75 billion campaign. With initiatives that span the globe, accelerating outcomes, we’re creating a better world right now. Learn more about our mission